The first point of contact potential customers have with your digital banking is the process of opening their first account. Know Your Customer (KYC) should be the time when customers slowly come to like your design and user experience. This is crucial now, when digital onboarding has reached new heights over the pandemic and branch visitation was minimized over health restrictions.

For the purposes of this blog, when we speak about KYC, we refer to digital onboarding, when a user becomes a customer. Not the long-term process/relationship with users throughtout their time as the bank's customers.

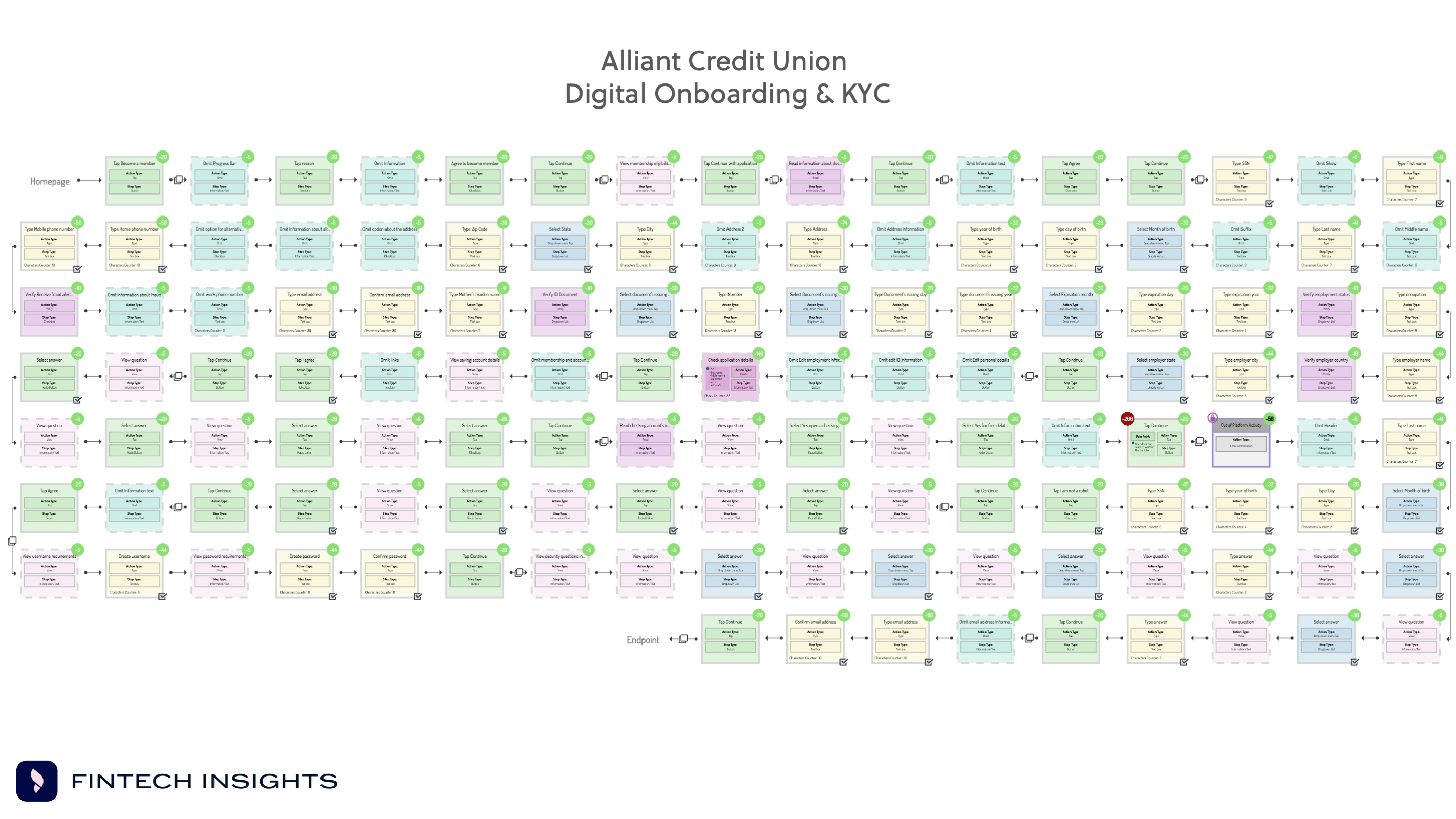

Many pages have been written about KYC. A few by us as well, ranking UK challengers and US Challengers according to their digital onboarding and comparing their whole KYC processes or discussing the KYC legacy US banks. Yet, despite the importance of KYC to making a great first impression to your customers, many banks make this an intricate and lengthy process that achieves the opposite. Instead of appealing to potential users, they manage to tire them before they have even opened the account, and in worst cases force them to abandon their process.

Having analyzed hundreds of digital onboarding processes for banks and fintechs worldwide through  , we have prepared a list for you of these practices that can turn customers away from your product.

, we have prepared a list for you of these practices that can turn customers away from your product.

Too many steps

The most detrimental issue to customer experience in a KYC process is its length. Customers expect their account opening with a new bank to be a smooth and easy process. However, for many banks the process can become quite cluttered with an excess of many steps, many of which can be covered by previous ones or removed completely.

These might include uneven in length steps in the process where customers have to input information in 4 different fields in the first only to be followed by the next step with 15 different fields to be typed in. It also includes several unnecessary information that customers need to omit such as offers/products for them or news (e.g., COVID-19 impact on the bank) and verifying information multiple times. All that is augmented in cases in which users will have to repeat the whole process if they discover they have made a mistake with their application instead of being able to correct one of the steps and not the whole process.

The result is a bloated KYC process that takes too long to be completed, is not UX-friendly for the customers and ultimately doesn’t serve the customers’ needs conveniently.

Type several times

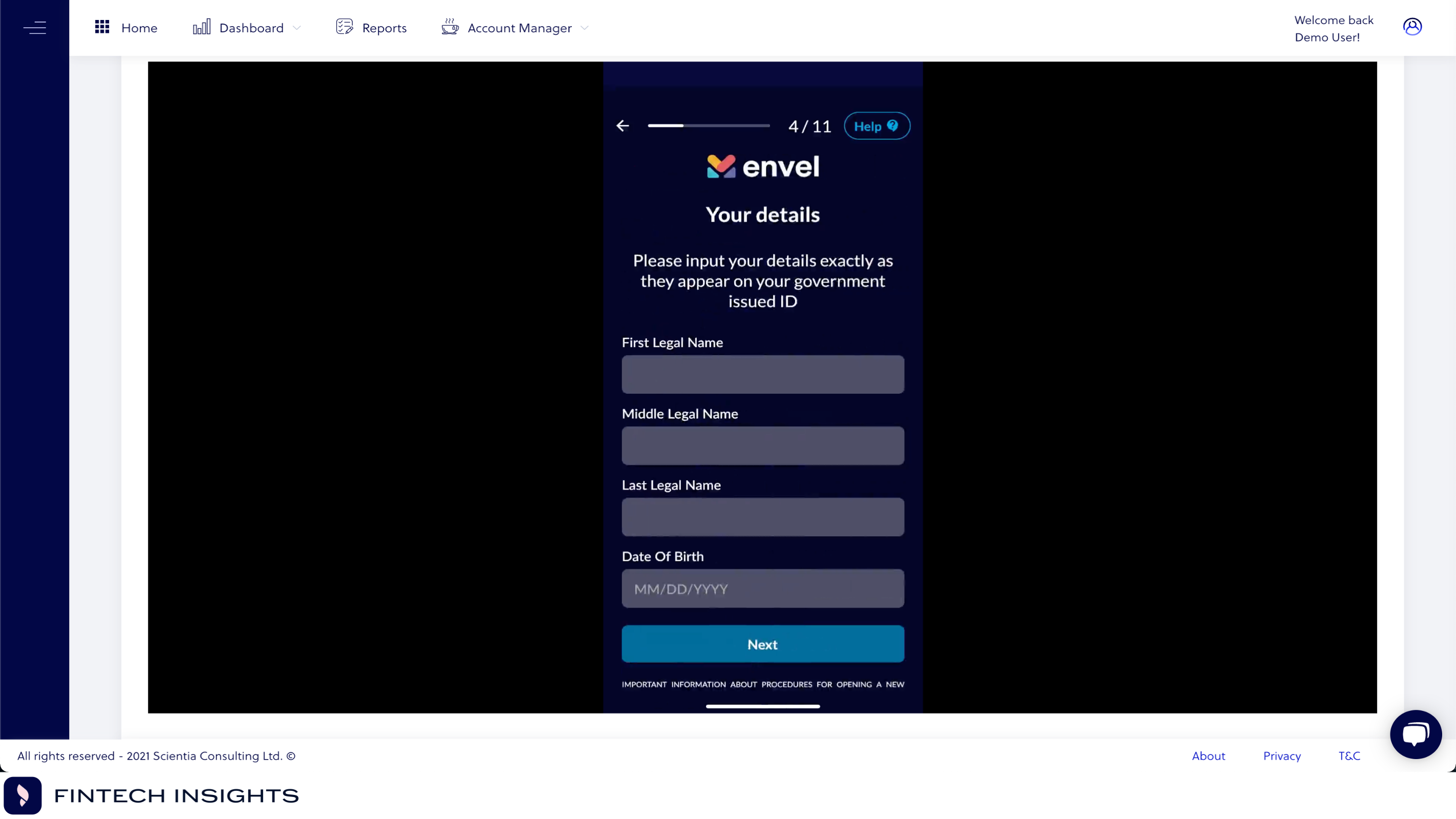

Another practice that makes customers dissatisfied with a bank’s KYC is having to type in too many times, especially information that is repeated or irrelevant. Typing several times is a major friction point for new users, even if it is for necessary elements of KYC (name and social security numbers), when alternatives (such as taking a photo of a passport and automatically inputting details) exist. Furthermore, they are dismayed when it is required for them to re-enter their email, or physical address again and again when this could be copied over by the digital banking application.

Customers, also, don’t wish to have their process of opening accounts be interrupted by answering survey questions like “how did you hear about us?”. To cap this all, many banks require their users to set up security questions, answers or both for their accounts. This practice seems outdated and could potentially be removed today where logging in can be safely completed through the use of a PIN number or user biometrics.

These repetitive or irrelevant questions can lengthen the process so much so that customers will have to take a break during the process or give up completely.

Disruption of the process

Another practice that leaves a negative first impression on customers is the process being disrupted. In this case, we include steps that halt the progresses such as customers waiting to receive a confirmation email which evidently may slow down the whole process. These out of platform activities – where customers have to navigate from the platform they started the application to another – include receiving and typing an sms or having to fund the new account with an amount from another one to activate it or even contact customer support.

Additionally, some banks require their new customers to complete the first stage of onboarding by creating their bank account to then return to set up their passwords and security. Instead of a single-stage process, they split it up into two which can be confusing for the users.

While including out of platform activities might be necessary for security and verification purposes for a new account opening, it is never a good practice to include multiple such steps. The users want convenient processes that don’t force them to swap between applications or pages, many times overcomplicating the process. It opens up the probabilities of error occurring during the process such as a webpage closing down by mistake or the mobile application malfunctioning due to increased background activity. Few customers won't be irritated by having to restart the process due to app closure and the chances increase that they might abandon the process altogether.

There are alternatives to authorize or verify details (e.g., through biometrics) but reducing the number of times users are requested to perform out of platform activities can be effective and help streamline the KYC.

No progress report

It goes without saying that when a customer sets out to open a new account they need this process to be as smooth and as easy as possible. They also need to know how long the process will take them to complete, so they know how much time they have to put in and what is their progress during the KYC. Here lies the need for a process progress bar that will inform users at which stage of the KYC they are and how many steps they have to complete in order to finish.

Many times customers that are unaware of how long a process is might start it and end up dropping out before its completion because they find that it’s too long. Or more frequently that they have not factored their available time to do it. Notifying customers early on of the steps needed and the time through a progress bar that continuously updates them on their journey makes all the difference to customer satisfaction and trust.

New customers will be more in favor of a bank or fintech that lets them know early on how much time they will have to invest for this process rather than finding out in the end or leaving mid-way. A feature as such should not be waived aside as an extra benefit of the KYC. It sets an early tone of trust and transparency as banks are letting their customers know what is going to happen and how long they will have to focus on the process. It finally allows them to feel they are in full control of the process, steadily moving from phase to phase instead of being ushered along in a process that they don’t know how it's structured.

Digital onboarding is arguably the most important process for new customer as it is the first crucial point of contact. A few years ago, this would be a customer entering through the door to one of the bank’s branches and sitting down to have a nice and helpful conversation with a clerk while they set up their new account.

However, the web or mobile application KYC represents today all that experience compacted into a single process through which people become familiar with your bank and turn into customers. It is the first touchpoint of the relationship customers will have with their bank.

How do you expect that relationship to go if the first meeting leaves a less than enthusiastic impression? To rephrase a few great words “KYC is king”.

Head over to and discover how you can build the KYC that makes sure your customers will start loving your digital banking!

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.