.png?width=320&height=180&name=unnamed%20(1).png)

The notion that customers own one bank account or are customers of just one financial institution reflects less and less percentages of the market. Recent research from FICO and Cornerstone in the USA has shown that 35% of consumers have more than one account while 42% of Millennials have two or more in different institutions.

The reality is that customers often own more than one bank account in different financial institutions. And that is due to the fact that financial institutions do not offer all features or serve all their daily needs through one digital banking channel. They might use one bank for saving money, another for sending money abroad or paying friends or investing.

Even if being the customer’s sole bank for their finances isn’t the full reality today, it is still crucial for banks to be the customer's go-to institution for their daily finances management. Customers using primarily one financial institution over others makes them prone to signing up and utilizing more banking products from them. They are more likely to remain long-term customers thus bringing in more profit for the financial institutions with an extended relationship.

The benefits of offering digital banking that customers will use daily are undeniable. But what are the features that can influence customers make a bank their go-to for their digital banking?

Using our digital banking research platform,  , and factoring in the UX of features offered worldwide, we prepared a short list of these offerings that make customers crave your digital banking.

, and factoring in the UX of features offered worldwide, we prepared a short list of these offerings that make customers crave your digital banking.

Security features

Customers set trust among the most important factors when selecting a financial institution. They need to be certain that their money will be protected. There is no more transparent way to achieve that than through ample and strong security features. Beyond setting security questions and passcodes, biometrics have proven to be an effective added feature as they require users to log in using their fingerprints, voice, or through iris scan.

Live videos or instant selfie pictures taken to complete a process (e.g. digital onboarding) is an excellent feature addition towards customer safety. These processes require their physical presence which and therefore it cannot easily be completed by another person rendering extra secure.

Imagine losing your phone, wouldn’t you feel more secure about your money if others had to use your fingerprint or scan your iris to login your bank account? Another interesting security feature has been introduced in new device pairing. Users need to re-take selfies or photos of their ID to prove it's them when pairing a new device.

Tip: Revolut requires users to take a selfie of themselves while pairing the new phone to verify they are them. Barclays on other hand has customers jump some hoops since they have to input several information and even use a card reader to pair.

Alerts

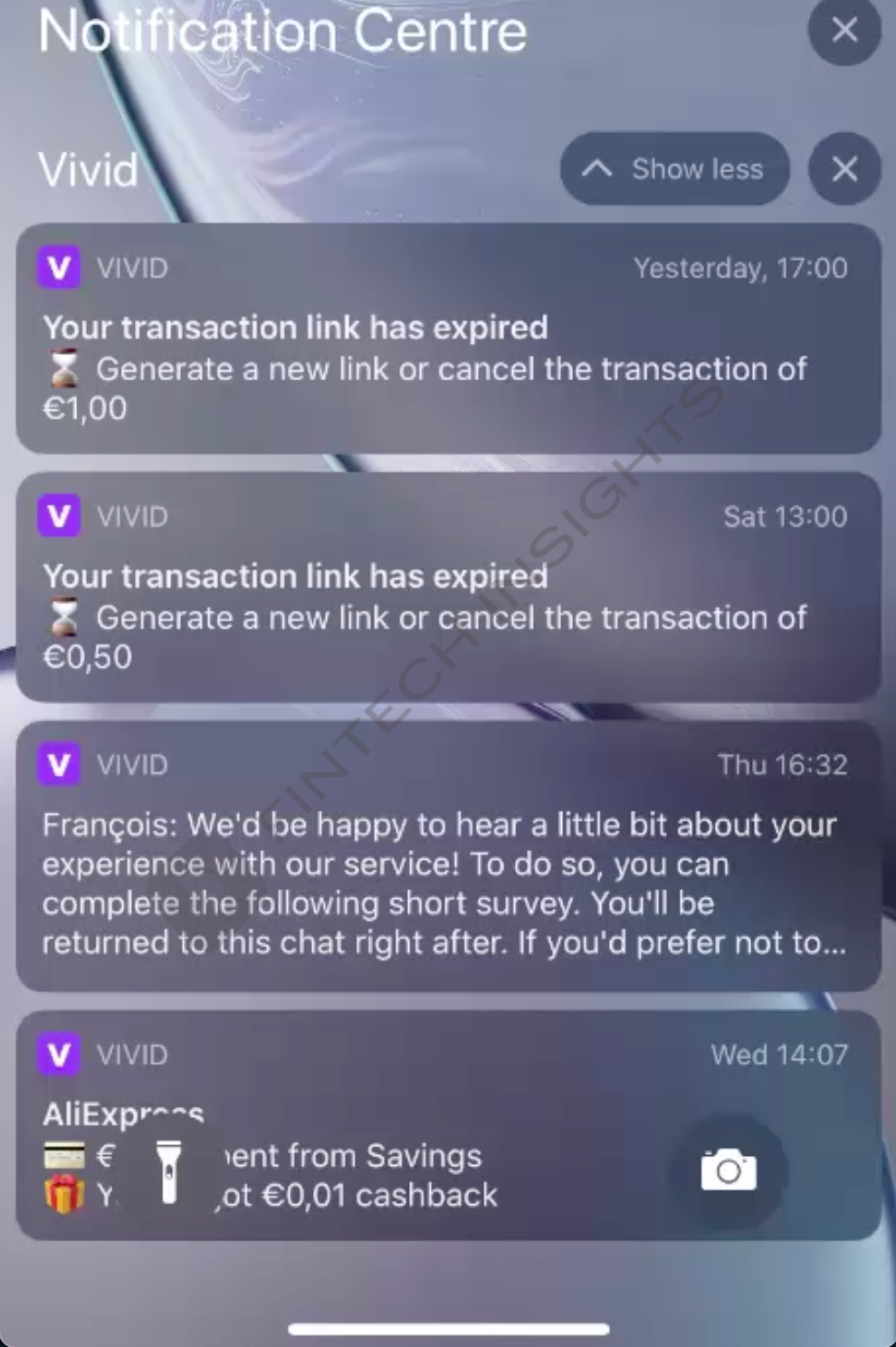

Having talked about security in their digital banking we had to also include alerts as well. As with security features, alerts allow customers to feel secure about their finances. They take the form of email or push notifications that inform users of various events. We include:

- alerts about the state of customer finances through (potential) low-balance or overdraft alerts,

- transaction alerts: card/account top-up alert, suspicious transaction, payments

- personal information change alerts

- security alerts (e.g., someone logged in from a different device).

Alerts provide customers the sense that they are always on top of their finances as they can be notified and take immediate action. In the past they would have to wait for a call to be told that something is wrong, which all of sudden could be quite frightening. Today banks use emojis and icons or even gifs to lighten the mood and make them quickly feel comfortable and speaking “their language”. They can instantly take control of the situation and rectify it without being close to a heart attack.

Tip: Vivid and Monzo customers receive push notifications about their transactions with the addition of emojis such as the dollar bill.

Support

"They don't offer that much, but I really appreciated the way they helped me when I needed it".

Support is fundamental for any customer-service relationship. It is important to offer such features that will aid customers when they need it. It could be as simple as offering supporting financial documentation (e.g., downloadable transaction reports, financial statements) that they can access and use momentarily.

Or more complex like tapping an intuitive support system that will provide answers to their questions and help them solve an issue they are facing. Such is the case with chatbots, integrated in the digital baking arsenal of a number of banks worldwide.

Through chatbots customers can

- receive helpful information about any process,

- be guided on how to solve an issue step-by-step

- be navigated to other parts of the application as a solution to a question,

- be shown community discussion threads

- contact a live agent.

Tip: Revolut offers quite an intuitive support chatbot. Customers ask a question and then they can either be directed to a community blog with the solution, or to another part of the app. They also the option for a live chat with a customer support agent.

Debit card protection

Debit card management has always been a critical customer need. With contactless payments and online shopping steadily rising over the past years and the pandemic accelerating the speed of that, the increased risk of fraud and security breach has heightened the need for extended card management. Customers need to be able to protect themselves.

The quickest way for them to do that is by getting rid of the “diseased limb”. We are talking about blocking or canceling a debit card when a suspicious transaction has been understood or when it is stolen or lost. But they should be allowed to reinstate their debit card once it is safe to use or order a new one.

In addition a few banks have introduced virtual debit cards which can be added into digital wallets so they can have access to their funds and continue their activities while waiting for the replacement card. These features enable them to quickly safeguard their finances but also go on with their daily shopping almost uninterrupted by the anxiety-inducing event of having their card compromised.

Tip: Chime offers a temporary virtual card for users until the debit which they have cancelled arrives.

Wealth management

One of the most challenging tasks for people is trying to manage their money. Earlier we discussed the 8 features that simplify daily money management. Banks should be providing as many ways as possible for customers to feel in control of their money. A few examples of features that have been introduced by banks for that purpose and that will help make a financial institution the customers' go-to-bank include:

- expense analytics and reports that allow them to monitor, understand and organize their spending

- budgeting tools with which they can set a budget for every expense they have

- notifications when they exceed their budget

- saving tools that help them achieve their goals like set saving goals, save the spare change and automatic allocation of funds etc..

These features can put customers in prime position to better manage and organize their finances and show that a bank puts their customers' wellbeing at the heart of their products.

Tip: Envel provides the Autopilot feature. Through that, customers – who have input their income and indicated their spending on utilities, rent, mortgage and subscriptions – will have their spending calculated and be proposed a budget for these. This budget will be automatically allocated to the 4 relevant envelopes (Cash, Emergency, Bills, Vault) which are created when opening their checking accounts. Customers can also set a daily, weekly or monthly “Guilt free Spending Limit”.

Financial institutions should be aiming to serve customer needs as completely as possible through their digital banking offerings to become their go-to-bank for their daily banking. Incorporating these 5 feature sets into their arsenal is surefire way towards becoming a customers' primary bank. Each of these correspond to fundamental customer needs: safety, security, convenience, sense of support and control and desire to benefit and improve their financial situation. They are necessary then to be included in bank's digital banking capabilities if it hopes to draw in customers and earn their trust and loyalty.

Explore

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.