The state of US payments

Before FedNow's July 2023 launch, US bank transfers typically took up to 4 business days.

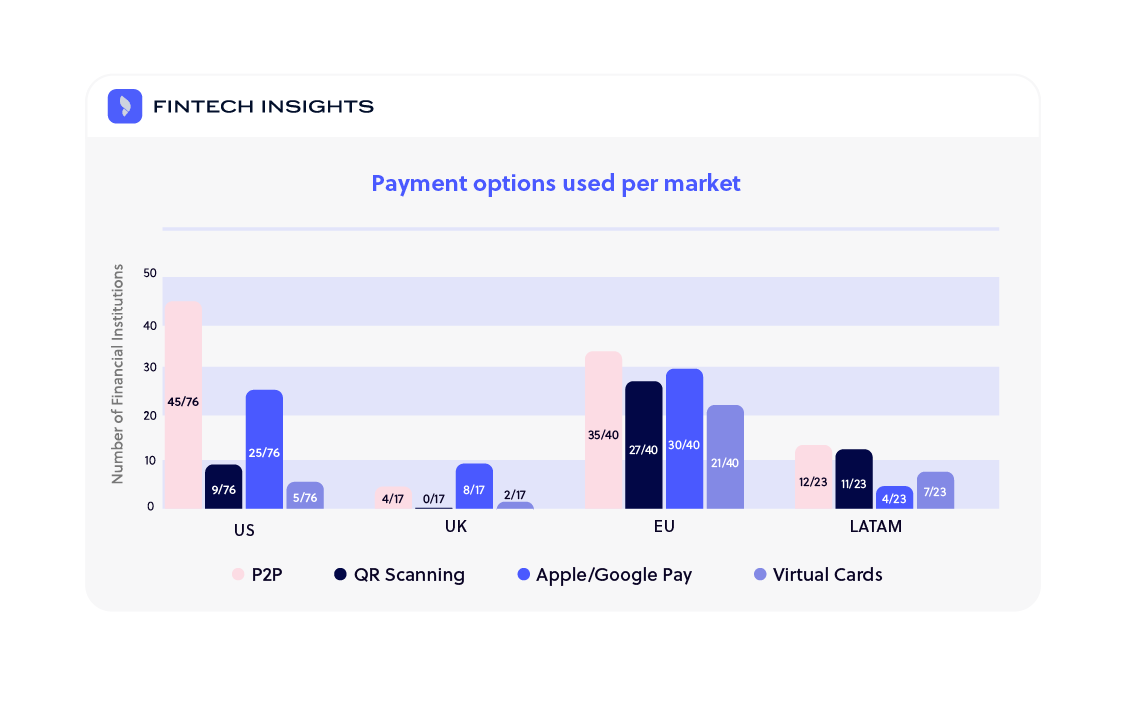

As a result, P2P payments — instant transfers using the recipient's email, phone number, username, or geolocation — are extremely popular. 44% of respondents in a 2022 study said they used them at least once a week. So it's no surprise that 45 of the 76 US banks in our database have P2P capabilities.

While any bank or credit union can now use FedNow for instant transfers, consumers typically stick to what they're familiar with. FedNow may supersede P2P in time. But US players that don't offer the latter will lag behind, at least in the short term.

What other payment methods are popular in the US?

US banks and challengers also offer payments through scanning — using QR codes — virtual cards, and e-wallets.

e-Wallets, primarily Apple Pay and Google Pay, are the second most common payment capability in the US, with 25 out of 76 banks offering it.

Given their popularity — 56.3% of respondents in a 2022 survey said Apple Pay or Google Pay was their preferred online payment method — we'd have expected more banks and challengers to have the capability.

Similarly, virtual cards are gaining traction, especially for employee expense management. So the 5 players offering the capability have a significant competitive advantage.

Maturity and convergence: the UK market

Where, in the US, P2P filled a significant market gap, UK consumers have long been accustomed to instant transfers. Faster Payments, the British version of FedNow, launched in the UK in 2008.

This probably explains why only 4 out of seventeen UK firms in our database offer P2P payments. Put simply, because Faster Payments already offers a secure, convenient way to make instant transfers — and it has been around for a long time — there's little incentive for consumers to use P2P (or for banks to offer the capability).

UK banks are also short of other alternatives.

Given the ubiquity of contactless, it seems strange that only 8 out of 17 offer Apple Pay and Google Pay. But, in reality, most consumers tap their cards. Only 37% use Apple Pay regularly, and only 22% use Google Pay.

With just 2 banks offering virtual cards and none offering scanning, the UK lags behind other markets.

Virtual cards are increasingly popular in the business expense management space, so the banks that offer it have a competitive edge. But while QR codes are popular in marketing, research suggests there's little interest in using them to pay.

EU payments: a diverse landscape

EU bank transfers are instant. But banks also offer a wide range of alternatives.

The vast majority have P2P and eWallet capabilities — 35 out of 40 and 30 out of 40 respectively. Scanning and virtual cards are also more widely available than in other markets. 27 of 40 EU banks offer the former, and 21 offer the latter.

If there's so much choice, this is probably because payment preferences are much less homogenous in the EU than in the UK or US. And catering to a diverse customer-base requires a diverse set of features. Case in point, only 20% of Germans regularly use e-wallets, while, in Spain, 37% do.

Latin America: an emerging digital powerhouse

Mistrust of legacy payment rails means digital alternatives are essential for succeeding in Latin America. But the region's banks have some way to go to meet expectations.

Only 11 out of 23 offer scanning, for instance, despite QR codes accounting for 112.8 million payments in the second half of 2022.

Banks are similarly behind on P2P and eWallets. eWallet use is expected to grow by 20% a year between now and 2025, for instance. But only 4 banks have the capability.

P2P payments are a similarly fast-growing area. But while more banks offer it than eWallets — 12 out of 23 — half the region's banks don't.

In payments, one size never fits all

It's a universal truth that you can't succeed in business without a good grasp of your market's needs. But it's especially so in payments.

Payment preferences evolve out of practical realities, but quickly become ingrained. Banks that understand and cater to these preferences earn loyalty and trust. And those that don't risk being left behind.

Interested in learning more about the must-have payment options used worldwide?

Book a free demo of FinTech Insights.

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.