A tale of two narratives

While Monzo explained its US exit as: "a deliberate, strategic decision to focus on scaling in our home market and Europe," the broader context reveals a more nuanced picture.

It's certainly not a coincidence that Monzo announced its exit in March 2026, three months after it obtained an EU banking license.

But it's also true that in May 2025 — less than a year earlier — Monzo stated in its Annual Report that it intended to continue its US expansion.

So what changed?

Cost is the obvious place to look. Industry observers estimate it costs about $300 to acquire a single American customer — three times higher than the global average — which means scale is critical.

This is exactly the reason why HSBC divested itself from its US retail banking business. As HSBC's Group Chief Executive Noel Quinn said, very bluntly, these operations

"...are good businesses, but we lacked the scale to compete."

The regulatory landscape also matters.

The US is an outlier among large, developed countries, in that it doesn't have a single federal banking regulator. Instead, it operates a dual system, with multiple federal agencies and fifty state-level regulators all involved in supervision.

This patchwork leaves an overseas player that wants to enter the US with two basic choices:

- Obtain approval in every single state in which it intends to operate — a prohibitively expensive and extremely operationally complex approach, even for a well-funded firm like Monzo

- Gain nationwide access by obtaining a banking charter, purchasing an already established bank, or relying on a partner-banking model

Monzo applied for a banking charter in 2020, but withdrew its application in 2021 when it became clear it wouldn't be approved. It then continued its operations via a partner-banking model.

The latter has the advantage of being quick, because it enables a firm to piggyback on an already established bank's infrastructure and expertise, but it comes with the trade-off of less control over the product lineup.

Monzo's place in the US market

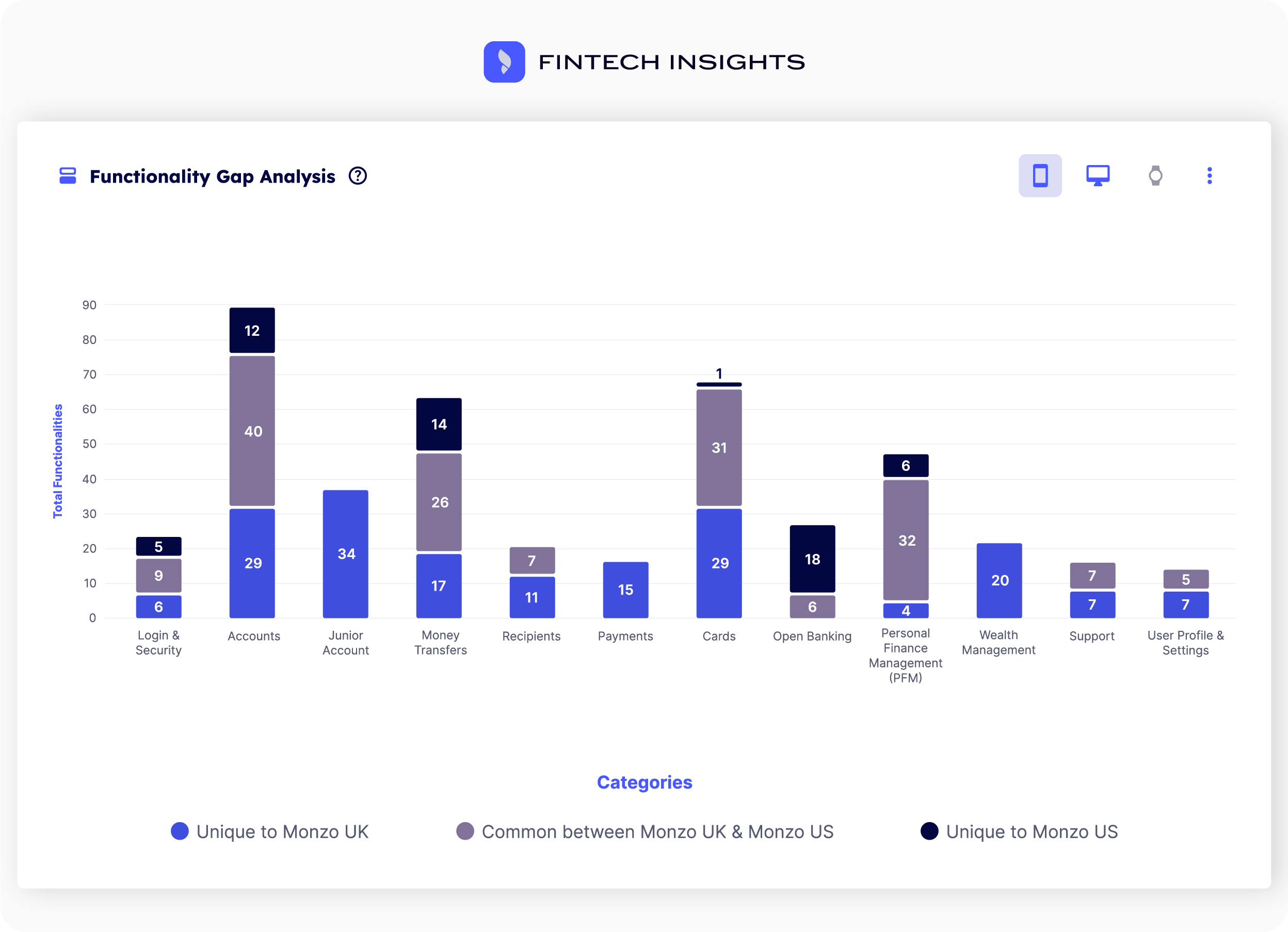

To investigate the challenges faced by Monzo specifically and other European banks and challengers looking to expand to the US more broadly, we used our digital banking research platform FinTech Insights to compare Monzo's UK app to the US app so as to pinpoint which features the latter was missing.

We then focused on the gaps that are important in the US context:

- Lending products

- Mobile check deposit

- Transfers (domestic and P2P payments)

- Bill payments

- Certificates of deposit

- Wealth management

Here's a look at why Monzo US might not have offered these functionalities, and the implications for other European banks looking to enter the US.

Lending

Where the EU's single rulebook harmonizes prudential requirements across all 27 member states, the US is a regulatory patchwork. Licensing requirements, interest‑rate limits, and key elements of consumer protection vary by state, with federal rules from multiple supervisors on top.

In theory, partnering with a US-chartered, FDIC-insured bank should make it possible to navigate this challenge.

In practice, partner banks are the legal lenders and hold the risk, with overdrafts in particular having become a major regulatory focus. As a result, they're increasingly selective about supporting new market entrants.

This was likely the case for Monzo, and it will probably be a hurdle for many other challengers that, despite their European success, are yet to prove themselves in the US.

Interestingly, Revolut has bucked this trend, and offers personal loans via its partner bank.

Mobile check deposit

A quirk of the US banking market is that checks are in wider use than they are in Europe or most other countries around the world.

In a 2021 study, 5.1% of all cashless payments in the US were checks — the highest of the countries surveyed. At 4.1%, France was the closest European country in terms of usage, while, in the UK and other EU countries surveyed, check payments were negligible.

For this reason, mobile check deposits — or remote deposit capture, as it's known in the US — are a must-have for any bank or challenger that's serious about building a US presence. But the vast majority of European firms don't have the capability, for the simple reason that they've not needed it to date.

In order for an EU firm to support this feature in the US is through a partnership with US clearing vendors. The challenge with this approach is that, because partners are on the hook for any losses when customers cash fraudulent checks, they impose strict conditions and require aggressive fraud detection processes.

Transfers

For a financial institution to successfully compete in this area, it must support both ACH and P2P payments.

ACH, the primary bank-to-bank network, uses routing numbers and account numbers, rather than IBANs. Switching identifiers is relatively minor on its own, but it creates a different operational reality to the one under SEPA: new dispute and return codes, different risk patterns and hold policies, and the need to juggle overlapping domestic payment rails.

Because ACH is batch‑based and typically settles same‑day or next‑day rather than in real time, most consumers use P2P for everyday transfers.

With $1.2 trillion processed in 2025, Zelle is emerging as a key P2P player. The catch is that it's a closed network, owned and operated by a consortium of major US banks, and, so, only accessible to US-domiciled, FDIC-insured firms.

Here again, even if a firm does gain access to Zelle through a partner bank, the vetting process and ongoing requirements around fraud prevention, identity verification, and transaction monitoring can be hard to sustain in the early stages.

Bill Payments

Like transfers, US bill payments are also a patchwork, with digital payments sitting alongside paper-based processes.

It's not unheard of, even in 2026, that banks mail checks to smaller merchants. This means that not supporting check issuing — either directly or through specialized partnerships — puts you at a disadvantage.

Digital bill‑pay products typically use ACH, and this requires the right operational and compliance setup. Validating accounts, juggling differing state-level consumer protection rules, and other complexities is far easier for a US incumbent than it is for a European newcomer.

Certificates of deposit

While, in theory, any European bank or challenger could offer certificates of deposit — the US version of a fixed-term savings account — this would be extremely difficult to market if not covered by the FDIC, which guarantees up to $250,000 per depositor.

Many firms get around this by entering into an arrangement where they handle the customer experience while a US-chartered, FDIC-insured partner bank holds the deposits on its balance sheet.

Even then, the challenger still has compliance obligations that require US-specific infrastructure and expertise.

Wealth management

Building a comprehensive, high‑end wealth management product offering requires legal, regulatory, and tax expertise most European firms don't have.

Some European incumbents are finding room at the top end of the market by focusing on ultra‑wealthy clients. The UBS-Credit Suisse merger, for instance, has strengthened the Swiss multinational's US wealth management footprint in a way that enables it to operate at scale.

Of course, this kind of play isn't feasible for many European firms. That said, when it comes to retail offerings, the bar is still relatively low. And, with demand for digital-first wealth management services on the rise, there's an opportunity for firms to come in and close the gap.

The UI question

Core product features aside, it's also worth considering a softer but just as important layer: the user interface.

The hallmark of European firms' UI design is a modern, playful, highly customizable interface.

US banks, by contrast, skew more conservative, with muted color palettes and less customizability.

And, while some US challengers, like Chime and SoFi, do adopt a more modern approach, it's arguably still more restrained than that of European firms.

Might European banking apps feel so unfamiliar to US customers as to be off-putting?

At the risk of crossing the line into pure speculation, it seems unlikely that design on its own would make or break a market entry. But it's another layer of friction on top of the regulatory, infrastructural, and product hurdles.

US entry: Is it worth the risk?

For European banks and challengers, the siren song of the US can be hard to resist.

Success in the US can be worth more than several European markets combined. And, unlike Europe, where the language, culture, and consumer expectations can be different even within relatively small distances, the US is relatively homogenous.

But if the upside may seem too good to pass up, Monzo's exit shows that being already successful in the UK is far from a guarantee you'll make it in the US.

Sometimes, doubling down on a profitable home market and a harmonised European playing field may be more rewarding than tempting fate across the pond.

Want to dive deeper into the US digital banking market?

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.